When to use (and not use) the Box-Cox Test to determine the optimum transformation for your data.

There are four ways to remedies in play to deal with non-trivial data:

1)Outlier detection

2)Parameter Change detction

3)Determinstic changes in the error variance (ie variability in the errors is not related to the level of the series)

4)Box-Cox(ie Power) Transfromations where the error variance is related to the level of the series

The choice of these remedies all have their positives and negatives. Some software IGNORES the richness of possible remedies. For example, if you couldn't implement 1,2,3 then you might have to rely upon on 4. So, sometimes you are stuck with your software. Here is an example of Quartic reciprocals "found" to be optimal, but of course the analyst didn't have access to alternative, simpler remedies.

The Box-Cox test premises that the model in place is the best model and that the parameters of the model are invariant over time. Furthermore, it is assumes that the variance of the errors does not have structural breaks or can be described by an ARIMA process. Additionally, the assumption is made that the errors from the model are free of Pulses/Level Shifts/Seasonal Pulses and or Local Time Trends which of course they likely won't be.

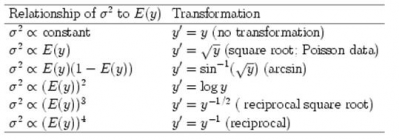

IF and only IF all of this is true then the Box-Cox test will yield the best lambda or power transformation. Review the following figure to better understand the implications of the “best lambda” as it decouples the relationship between the and the Variability of the errors and the Expected Value. For example, note that a log transform is a lambda of 0.0 while a square root transform is .5.

You have the option(option =2 when running) which is unique in that all of the items listed above will be addressed in the process, to provide a list of trial lamda's which are then evaluated. This option is when you might have a Note that with our automatic option (option -1), logs are the only transformation evaluated.

Some example transformations